Summary

Highlights

The US has seen some mixed macro data around inflation and labour markets, opening a debate on Fed’s future policy actions.

Weak US employment data and Chair Powell’s recent comments have led the markets to believe that a September rate cut is a done deal.

We think the Fed would not want to be seen as succumbing to political pressure and will prefer to maintain its data-dependent approach.

In this edition

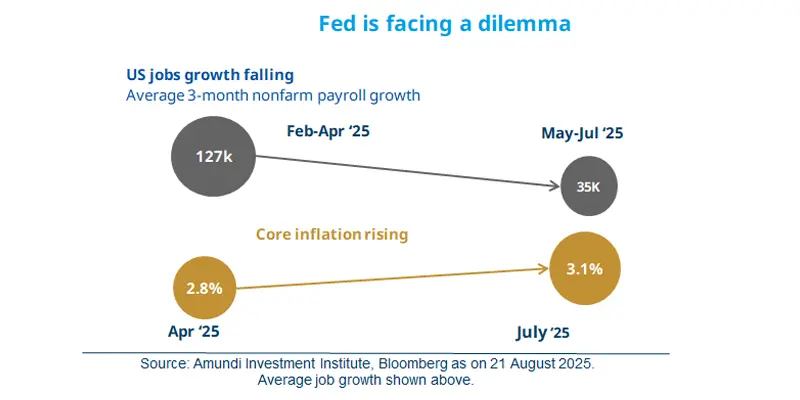

Macro data over the summer has heightened the debate between whether the Federal Reserve should reduce its monetary policy rates or wait for more clarity on inflation and labour markets. The US has witnessed a deceleration in average monthly job creation to around 35,000 for the past three months. On the other hand, core inflation (inflation excluding food and energy prices) has picked up and higher tariffs have been announced. Latest views from the Fed outline that many Fed governors acknowledge both these risks. However, most see inflation (partly due to import tariffs) as a bigger threat to consumption. In addition, at his recent Jackson Hole speech, Fed Chair Powell indicated the Central Bank is open to cutting rates. While the direction of policy seems clear in the near term, the market will continue to assess incoming data and its impact Fed’s actions.

Key dates

27 Aug China industrial profits, Germany retail sales | 28 Aug Bank of Korea policy, EZ money supply, US GDP |

29 Aug US core PCE July, ECB inflation expectations, India GDP |

Read more