Summary

Highlights

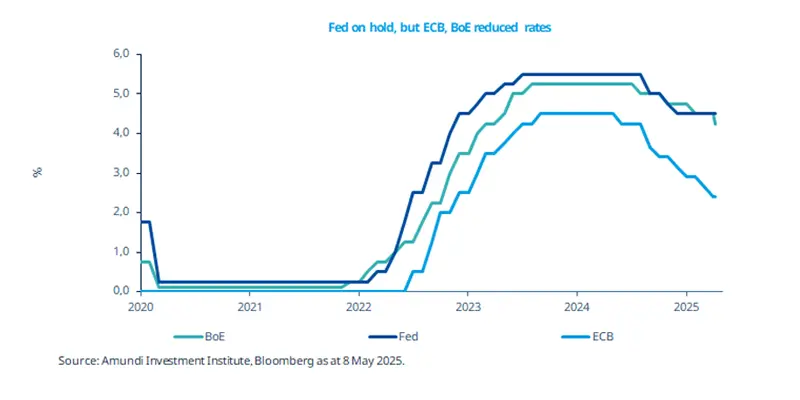

The Fed remained in a ‘wait and see’ mode, whereas the BoE and ECB (last month) cut interest rates in their latest meetings.

This policy divergence is a result of higher consumer inflation expectations, which the Fed likely considered in its latest decision.

In contrast, the ECB faces limited risks on inflation, for now. This calls for a global approach to asset allocation.

In this edition

The Fed refrained from cutting rates in its latest policy meeting, as it awaits more clarity on the impact of tariffs on inflation and consumer confidence. In contrast, the ECB and the BoE recently reduced their policy rates. The US economy contracted slightly in the three months ended March, marking the first contraction since Q2 2022. We believe the Fed’s repeated assertion that the economy is robust contrasts with weak soft data (such as surveys) and elevated uncertainty about both growth and inflation. We expect substantial rate cuts by the Fed later this year, as weaker growth outweighs transitory inflation pressures. A tariff-induced recession is not our base case, but uncertainty will remain high.

Key dates

13 May US CPI, Germany ZEW survey, UK unemployment rate | 15 May US retail sales, PPI, industrial production, EZ industrial production, UK GDP | 16 May US housing starts and building permits, US University of Michigan Sentiment |

*Diversification does not guarantee a profit or protect against a loss.

Read more