Ongoing conflict lifts inflation expectations

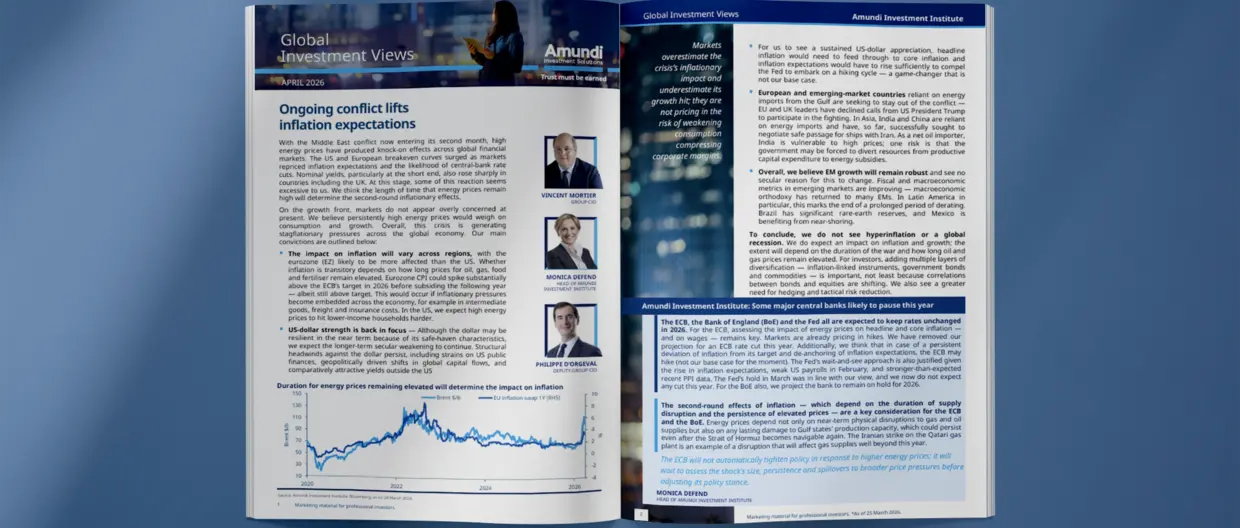

With the Middle East conflict now entering its second month, high energy prices have produced knock-on effects across global financial markets. The US and European breakeven curves surged as markets repriced inflation expectations and the likelihood of central-bank rate cuts. Nominal yields, particularly at the short end, also rose sharply in countries including the UK. At this stage, some of this reaction seems excessive to us. We think the length of time that energy prices remain high will determine the second‑round inflationary effects.

On the growth front, markets do not appear overly concerned at present. We believe persistently high energy prices would weigh on consumption and growth. Overall, this crisis is generating stagflationary pressures across the global economy.

Our main convictions are outlined below:

• The impact on inflation will vary across regions, with the eurozone (EZ) likely to be more affected than the US.

• US-dollar strength is back in focus — Although the dollar may be resilient in the near term because of its safe‑haven characteristics, we expect the longer‑term secular weakening to continue.

• European and emerging-market countries reliant on energy imports from the Gulf are seeking to stay out of the conflict — EU and UK leaders have declined calls from US President Trump to participate in the fighting.

• Overall, we believe EM growth will remain robust and see no secular reason for this to change. Fiscal and macroeconomic metrics in emerging markets are improving — macroeconomic orthodoxy has returned to many EMs.

Continue reading the full document

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 2 April 2026. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results.

Date of first use: 2 April 2026

Doc ID: 5343571