Convictions

The strong appeal of fixed income in an uncertain environmen...

Explore why fixed income stands out in an uncertain environment, with attractive yields, broad opportunities and regional diversification.

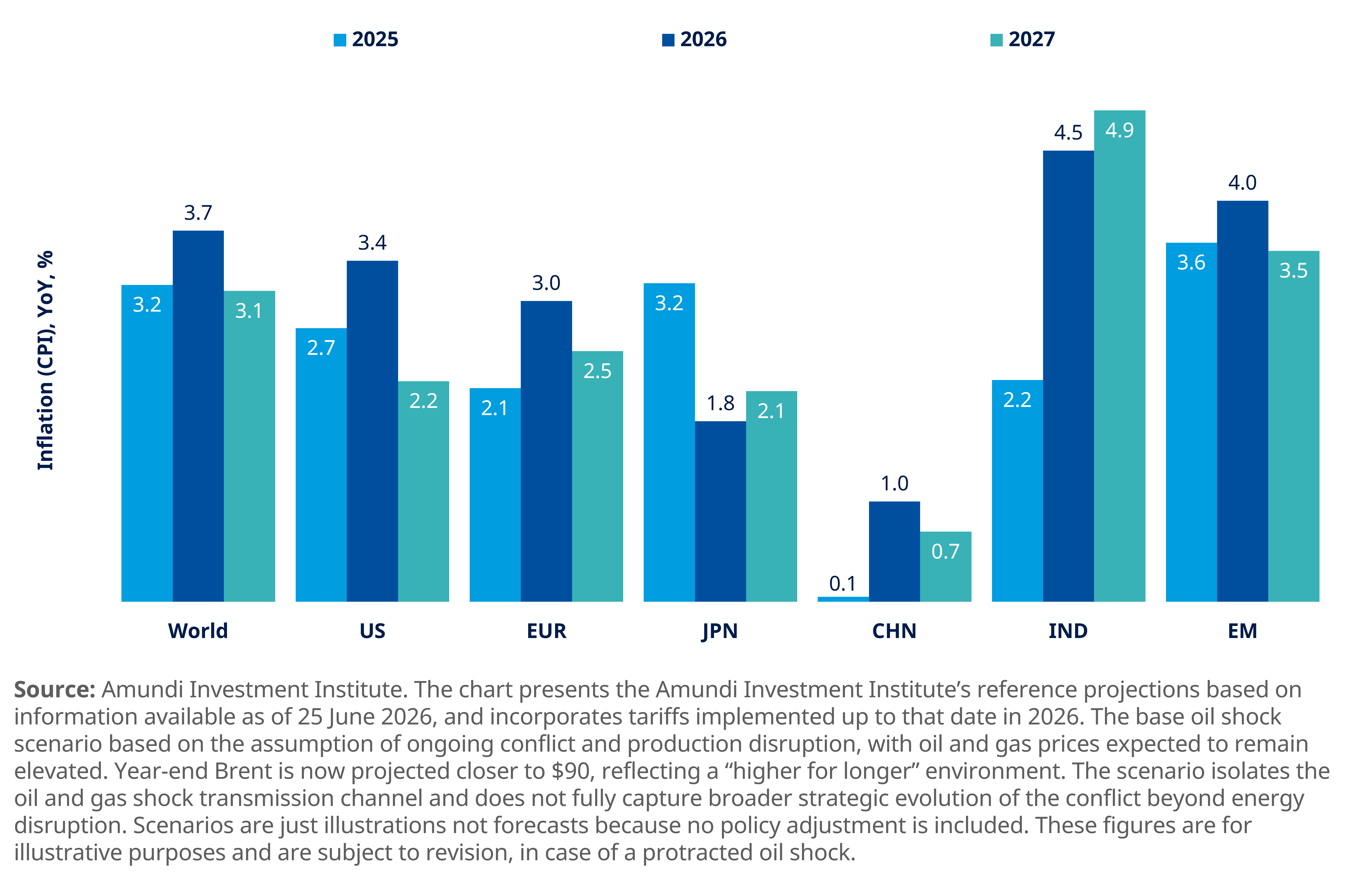

The first half of 2026 has reinforced the view that this is not a standard late-cycle environment. Geopolitical shocks are driving cost pressures across supply chains and corporate margins, while artificial intelligence (AI) remains a strong earnings driver across regions and sectors.

At Amundi, we see four key themes that stand out for investors: the resilience of the global economy to the energy shock, the credibility of policy response amid higher debt and constrained central banks, the US mid-term elections and its fiscal and regulatory implications, and the continued broadening of the AI supercycle.

Amundi Investment Institute's growth outlook

This backdrop calls for a selective, diversified*, and protective approach. Central banks’ policy remains a key watchpoint, with investors no longer able to count on a dovish pivot to support markets; asset allocation should therefore focus on selective long-term growth opportunities:

Government bonds remain important income providers in portfolios, but their diversification* role is challenged by higher inflation risk and uncertain monetary policies. We favour long-term real rates, inflation-linked bonds and investment grade credit, mainly in Europe, while relative value opportunities across regions should increase.

While markets have proven resilient, this should not be seen as broad strength. Sector selection will be key in the second half of the year, as pricing power, supply chain relocation and a supportive policy backdrop favour industrials, utilities and financials. AI opportunities now extend across the full value chain, but investors should remain mindful of market concentration, leverage, and growing volume of IPOs.

Three structural shifts will continue to drive opportunities: the push for strategic autonomy, the broadening of AI into industry, and geopolitical fragmentation. As many asset classes remain exposed to inflation and potential AI disappointment, investors should focus on real and private assets, gold, and FX hedges.

Higher yields have improved the case for bonds, but flexibility remains essential to capture income. High debt levels and uncertain policy paths make long-term sovereign bonds less attractive, while strong fundamentals make Euro IG and EM IG bonds particularly compelling, especially as they trade at a discount to their US counterparts.

AI is a structural driver of equity returns, but concentration risk remains a key consideration. US equities could be vulnerable to corrections if the Fed changes course. Investors should look across a broader opportunity set, from infrastructure providers to AI adopters across sectors and regions.

Europe’s strategic autonomy agenda is evolving into a multi-year investment cycle, with capital being allocated towards defence, energy security, AI infrastructure and industrial renewal. Private and public debt markets are playing an increasingly important role in financing capital expenditure across the region, while also broadening the investor base.

Emerging markets have evolved significantly over recent decades, and we see strong opportunities in those that are supply-chain winners, commodity exporters, or supported by credible policy frameworks. Investors should also look for sources of diversification* away from AI, such as exposure to natural resources linked to the energy transition. Nevertheless, caution is needed where dollar sensitivity is high and external balances are weak.

In a fragmented environment, greater emphasis should be placed on the real economy through private markets, as inflation increases the risk of traditional negative correlations weakening. Demand remains strong in areas linked to AI and the energy transition, such as data centres and infrastructure, but limited supply requires selectivity.

We see higher inflation, geopolitical volatility and USD debasement as key risks. Investors should consider a broader protection toolkit for their portfolios, including gold, FX, alternative investments and hedging strategies. We continue to foresee a potentially softer US dollar relative to EM and commodity FX. Demand for gold, as a reliable store of value, is expected to increase further, supported by limited mine supply and strong buying by EM central banks.

Source: Amundi Investment Institute Mid-Year Outlook 2026, “Power of endurance”, June 2026.

* Diversification does not guarantee a profit or protect against a loss.

Views and opinions are as of end June 2026 and are subject to change without prior notice.

Marketing material for professional investors only

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 20 July 2026. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results.

Date of first use: 20 July 2026

Doc ID: 5728517