In a nutshell

Markets remain dominated by developments in the Middle East. For now, investors interpret the impact of the conflict as a temporary inflation shock with limited impact on growth. The price of oil and wholesale gas has approximately surged by 40% and 60%, respectively. Government bond yields have risen across the curve, especially at the short end. The rates market has repriced inflation risks but not material growth risks. In this context of higher expected inflation, investors expect central banks to take a more cautious stance: market pricing currently implies one Fed cut in Dec 2026 with a reduced probability of a second cut, while the ECB is pricing one to two hikes.

The duration of disruptions to oil supplies is the key variable. The conflict could affect global growth through three channels: (1) higher prices for oil, gas and fertilizer; (2) increased uncertainty; and (3) repricing of risk (equities and credit). Europe and Asia are more exposed to energy price shocks, whereas the US — a net oil exporter — is relatively less exposed. However, the US economy is more vulnerable to financial market volatility. Philip Lane, the ECB’s chief economist, has warned that prolonged war in the Middle East and persistent disruptions to oil and gas supplies could cause a “substantial spike” in inflation and a “sharp drop in output” in the euro area. He emphasized that “directionally, a jump in energy prices puts upward pressure on inflation, especially in the near term,” and that such developments would be “negative” for growth. The magnitude of the economic shock would depend “on the breadth and duration of the conflict,” Lane noted, adding that “the impact would be amplified if it also gave rise to a repricing of risk in financial markets.”

The major central banks will hold their monetary policy committee meetings this week. We expect central banks to take a cautious, wait and see approach to policy changes. It is too early for central banks to draw definitive conclusions for monetary policy. We expect central bankers to highlight that the situation in the Middle East remains volatile and that the duration of the conflict is a key variable.

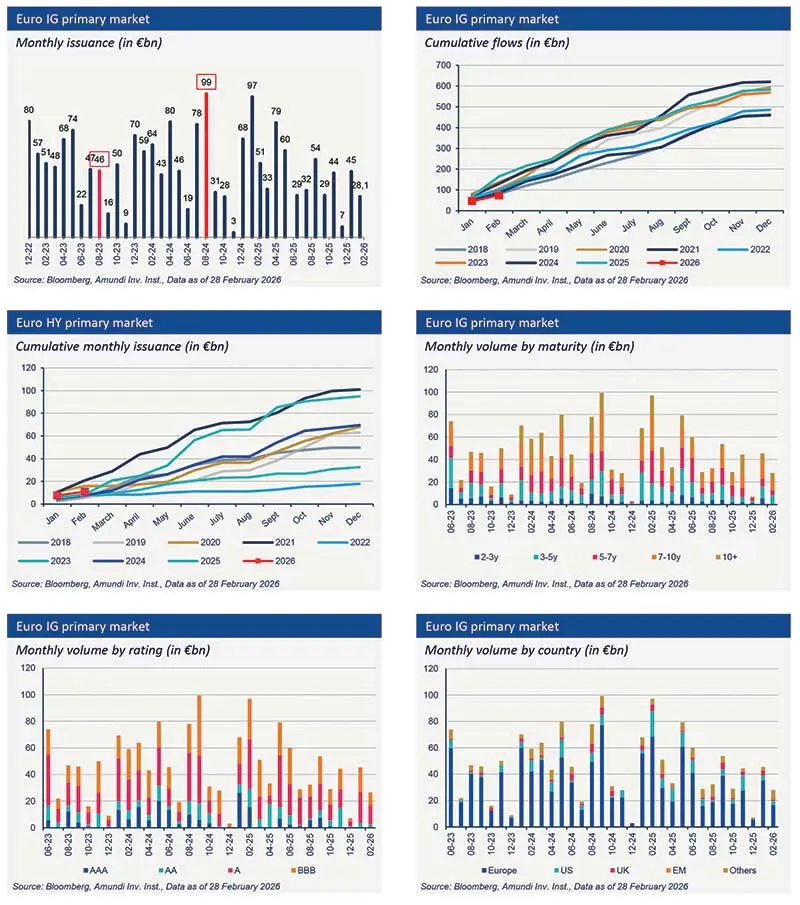

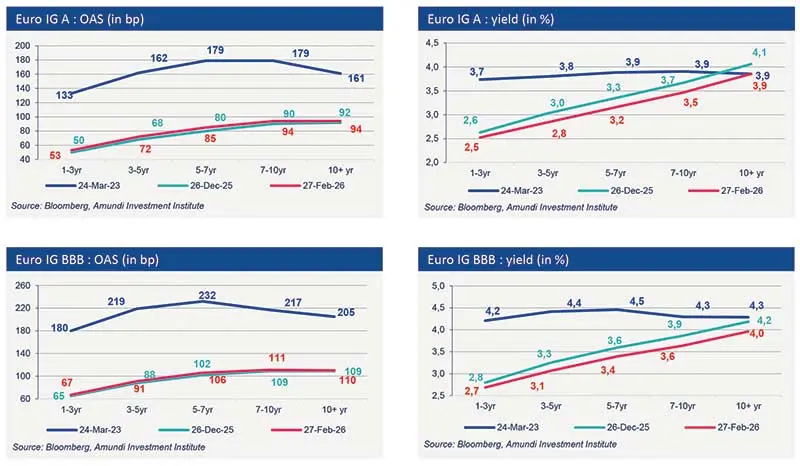

For credit markets, the current environment remains characterized by increased commodity volatility and a reassessment of monetary policy paths. Despite this context, credit markets remain relatively resilient, and spreads have widened only modestly since the beginning of February. Riskier issuers have underperformed. Euro investment grade (IG) spreads have widened by 18bp to 89bp and Euro high yield (HY) spreads by 51bp to 314bp. The same trend is observed in US credit markets: US IG (+20bp to 94bp) and US HY (+47bp to 327bp). However, this level of valuation does not reflect major concerns regarding global growth. Indeed, spread remain well below the peak reached following President Donald Trump’s “liberation day” tariff announcements (Euro IG: 125bp, Euro HY: 429bp, US IG: 121bp and US HY: 456bp). Moreover, companies remain active in the primary market despite the return of volatility. Euro HY Primary issuance in both IG and HY has slowed from the record levels reached in January, but the market remains open even for high yield deals. Investors are attracted by the opportunity of a higher new issue premium.

Primary market Investment Grade

Market data

Find out about our treasury offer