Summary

Highlights

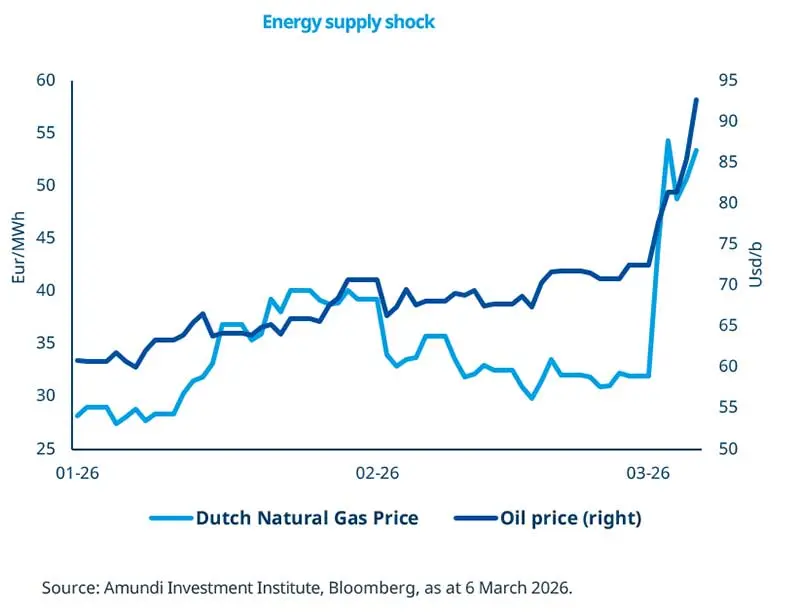

- The Iran crisis pushed oil and gas prices higher, raising concerns about higher inflation and weaker growth—especially in regions that rely on energy imports.

- In the absence of a material disruption to oil infrastructure and Hormuz traffic, we regard the current episode as a temporary oil shock with only modest implication for growth and inflation.

- Aside from tactical adjustments, from a long‑term perspective it is paramount to focus on fundamentals.

In this edition

Escalation in Iran transmits to the global economy and markets mainly through oil: the Middle East is a major oil and gas producer (c. 31% of global oil production and c. 18% of global gas production), and the Strait of Hormuz is a critical transit point, particularly for shipments to Asia, which receive almost 90% of the crude and condensate transported through the waterway. Oil shocks generally have uneven effects on economies: exporters tend to benefit while importers tend to lose out, with the intensity of the impact linked to magnitude and persistence of price spikes.

Over the weeks ahead, the oil-price outlook depends on the intensity and duration of disruption to infrastructure and Hormuz traffic. A short conflict with limited disruption could lead to a temporary oil price spike with limited impact on global growth and inflation. Central banks’ data dependent approach will likely result in a postponement of actions while they assess the growth-inflation mix.

Key dates

9 Mar CHINA PPI and CPI, Germany industrial production, Mexico CPI |

10 Mar Korea GDP, Japan GDP, South Africa GDP, China Trade balance |

13 Mar USA JOLTS Data, Consumer Confidence, PCE Price Index, GPD |

Read more