Key Takeaways

- Credit markets represent an attractive opportunity for clients seeking to increase portfolio stability in the current environment, thanks to solid corporate fundamentals and attractive yields. Its resilience has distinguished credit from other asset classes, including sovereign debt.

- A global approach allows investors to capture value across a wider universe, benefiting from regional and sector differentiation. Favourable opportunities are available across the US and Europe, in a range of areas including banks, defence and technology.

- Once tensions over Iran ease, attention is likely to shift back to AI and its disruptive impact, from the industries set to benefit from it, such as those involved in data centre production, to the sectors and business models most at risk. Future issuances, especially from hyperscalers, will increase the weight of these areas in the credit market.

Since the onset of hostilities in Iran, global credit has demonstrated notable resilience in an environment characterised by modest growth, which continues to support the asset class. Corporate balance sheets remain healthy, and although spreads are tight, yields remain attractive relative to historical levels, supporting ongoing inflows into the market.

A moderate growth and inflation scenario

The conflict in Iran has represented a supply shock for the global economy, with implications for higher inflation, weaker growth and heightened uncertainty. Oil prices have risen sharply, and the impact on growth has been transmitted through three main channels: uncertainty, higher energy costs, and tighter financial conditions.

Nevertheless, the scenario in which oil prices remain elevated for a prolonged period has diminished following the announcement of the ceasefire. At Amundi, our base case remains one of moderate pressure on both growth and inflation, as the probability of a more adverse outcome has fallen materially.

This environment should therefore remain supportive for credit, as modest growth should help keep inflation in check, while discouraging central banks from introducing aggressive policy tightening.

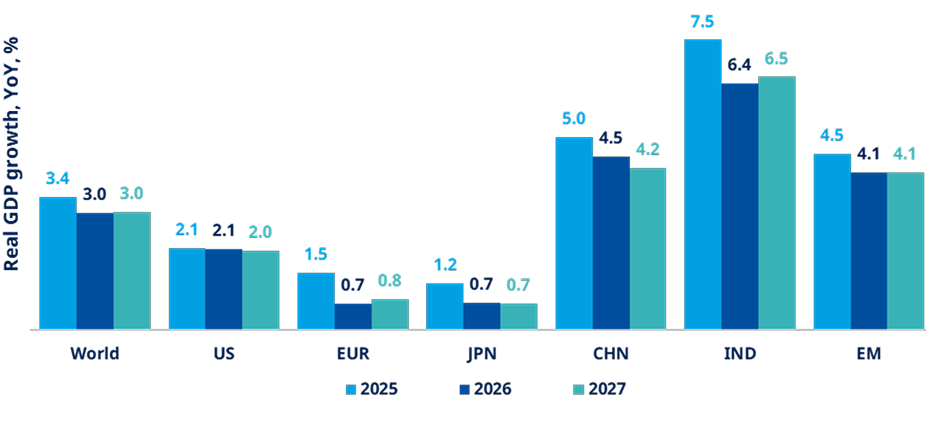

2026 growth: revised down and uneven

Source: Amundi Investment Institute. The chart presents the Amundi Investment Institute’s reference projections based on information available as of 15 May 2026, and incorporates tariffs implemented up to that date in 2026. The base oil shock scenario based on the assumption of ongoing conflict and production disruption, with oil and gas prices expected to remain elevated. Year end Brent is now projected closer to $90, reflecting a “higher for longer” environment. The scenario isolates the oil and gas shock transmission channel and does not fully capture broader strategic evolution of the conflict beyond energy disruption. Scenarios are just illustrations not forecasts because no policy adjustment is included. These figures are for illustrative purposes and are subject to revision, in case of a protracted oil shock.

Indeed, a further key consideration for credit markets is the outlook for central banks, namely how policymakers will respond to the inflationary impact of higher energy prices. In assessing the appropriate policy response, central banks are likely focus on three factors: the intensity of the shock, the extent of any second-round effects should higher oil prices spread through the broader economy, and the risk of inflation expectations becoming unanchored.

Credit has proved more resilient than government debt

To date, the market response to the conflict has been driven more by inflation and interest rate concerns than by credit risk. Credit spreads have remained resilient, whereas sovereign yields have been more volatile, rising across the curve and reflecting both higher inflation expectations and a reassessment of the central bank rate path.

There are also broader questions surrounding the fiscal outlook, with concerns about government debt, which has increased significantly in recent years. Government financing needs are now structurally elevated, driven by population ageing, the need to fund digitalisation and defence spending. As a result, many investors are questioning the long-term sustainability of sovereign debt.

By contrast, corporate fundamentals remain solid, with no increase in default rates and strong momentum. However, performance dispersion remains, allowing active managers to generate alpha through security selection and relative value analysis.

Looking at sectors, US companies delivered very strong earnings results in the latest reporting season. These positive outcomes have been driven largely by technology, supported by investments in AI and the build-out of data centres. While hyperscalers have traditionally had only a limited presence in credit markets, their representation is expected to increase meaningfully over the next five years.

We continue to favour banks, both in Europe and the US. In an environment of higher yields and steeper yield curves, banks’ net interest margins are strong, while their capital structures are very robust. There are also benefitting from regulatory changes, particularly in the US under the Trump administration.

Telecoms are another area in which we remain overweight. Here too, fundamentals are strong, and business models are defensive, with revenues proving highly resilient.

Defence is also attracting increasing interest, supported by higher spending commitments. In addition, the data centre boom is generating broader spillover effects across the economy, benefiting a range of sectors including utilities, construction companies and firms supplying cooling systems to data centres.

Selectivity remains fundamental, as not all areas are able to benefit from the current environment. For example, in the energy sector, it is still unclear whether companies will be able to achieve higher margins, while other industries remain under pressure, such as chemicals and automobiles. At the same time, attention on AI is expected to increase once tensions in Iran ease, and this could have a disruptive impact on some business models that are not able to adapt.

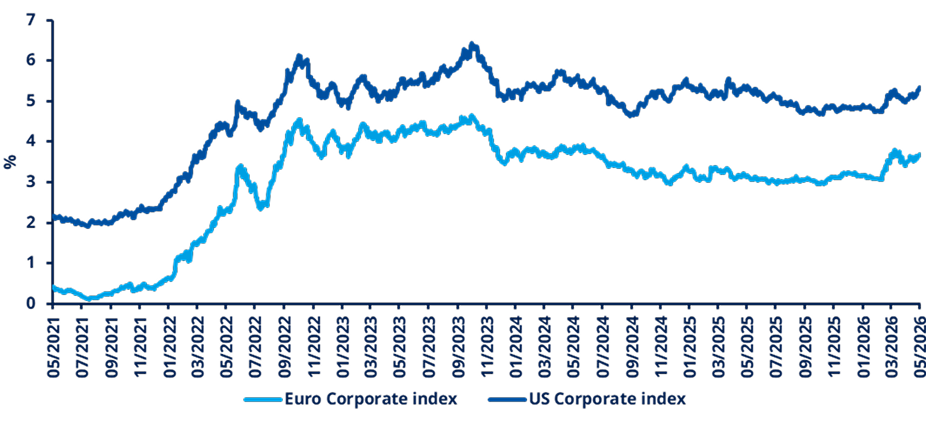

Compelling yields (YTW) in both US and Europe

Source: Bloomberg, as of 19.05.2026. Yield to worst (YTW): lowest yield an investor can receive on a bond if the issuer takes any action that is allowed under the bond terms. Indices used: Bloomberg Euro Corporate Unhedged EUR (LECPTREU) and Bloomberg US Corporate Total Return Value Unhedged USD (LUACTRUU).

Amundi Convictions

Source: Summary of views expressed at the most recent global investment committee (GIC) and discussions after. Views as of 20 May 2026. The table shows absolute views and are expressed on a 9 scale range, where = refers to a neutral stance. This material represents an assessment of the market at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research, investment advice or a recommendation regarding any fund or any security in particular. This information is strictly for illustrative and educational purposes and is subject to change. This information does not represent the actual current, past or future asset allocation or portfolio of any Amundi product.

Why Amundi for credit

With solid corporate fundamentals and attractive yields continuing to draw investor interest, global credit has remained compelling in an environment characterised by considerable uncertainty. At Amundi, we believe this resilience is likely to remain a defining feature of the asset class in the months ahead, creating attractive opportunities for clients to access with the support of skilled asset managers.

Amundi is an established player in fixed income, currently managing approximately €830 billion in active strategies as of 31st December 2025.

The teams’ investment philosophy is designed to deliver consistent returns by navigating credit cycles effectively and capitalising on market inefficiencies. Their approach is agile, combining top-down and bottom-up analysis to adapt to changing market conditions.

Explore our fund offering

Amundi Funds Global Corporate Bond

Amundi Funds Euro Corporate Bond Select

Amundi S.F. – Diversified Short-Term Bond Select

Amundi EUR Corporate Bond Active UCITS ETF Acc

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 03.06.2026. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results.

Date of first use: 03.06.2026.

Doc ID: 5520863.