Key Takeaways

- Euro investment grade credit can represent an attractive diversification opportunity within global portfolios, supported by solid fundamentals and compelling yields.

- Active credit management enables dynamic portfolio adjustments, including across duration, credit quality and subordination - a strong advantage at times of volatility.

- Amundi is a leading player in Euro credit, with nearly 30 years of experience and approximately €380 billion in assets1.

Since central banks began withdrawing support from markets in 2022 to fight inflation, the era of “lower for longer” has come to an end. Interest rates have therefore become increasingly responsive to macroeconomic developments and, as a result, more volatile.

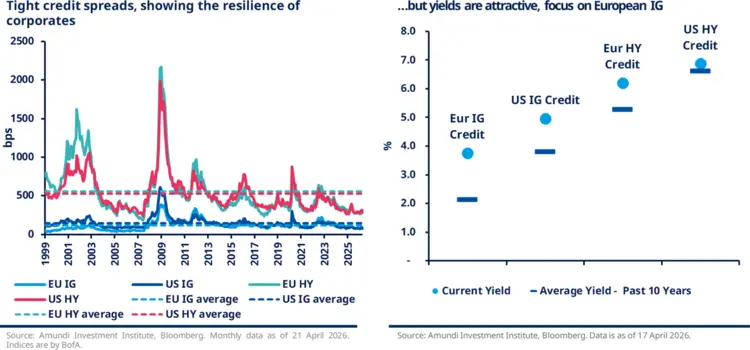

The Euro credit index1 has nonetheless navigated this environment well, thanks in large part to its composition. European companies are generally sound and characterised by well-managed balance sheets. Many have also adopted more conservative corporate strategies, including fewer mergers and acquisitions, lower capital expenditure and less aggressive growth targets.

More than one third of the Euro credit market is made up of financial institutions, which remain the main source of financing in Europe and therefore play a key role in channelling savings into productive investment. European banks have benefited significantly from the tightening cycle: in a higher rate environment, their net interest income and profitability have improved materially, supporting margins and stronger returns on equity. At the same time, their resilience has increased substantially over the past decade, thanks to the introduction of a robust regulatory framework and the establishment of the banking union, both of which have strengthened financial stability across the EU.

These strong fundamentals across corporates and financials, combined with higher yields, have helped stabilise credit spreads. Although spreads remain tight by historical standards - leading some investors to question the attractiveness of credit risk - the picture is more compelling when viewed through the lens of absolute yield. Current yield levels continue to provide adequate compensation for the underlying credit risk in European corporates.

The credit market still offers strong appeal, particularly EU IG

Why Euro investment grade credit as a diversification tool

This focus on absolute yield is not new. It has long shaped investment behaviour in the US credit market, where investors have traditionally been driven more by yield than by spread. In that respect, the Euro and USD investment grade (IG) credit markets are broadly comparable, although they differ in structure. The Euro IG market can therefore be seen as a credible diversification option for USD-centric fixed income portfolios, thanks to its distinct sector composition, shorter maturities and relative valuation opportunities.

| Euro Investment Grade Credit 3 | USD Investment Grade Credit 4 | |

| Market depth and liquidity | Smaller than USD IG, but highly developed and liquid | Larger and deeper global market, with broader issuer base and stronger overall liquidity |

| Sector mix | Higher weight in financials (~44%), followed by consumer discretionary (~10%), utilities (~9%), and industrials (~8%) | Higher weight in financials (~33%), followed by healthcare (~11%), utilities (~10%), and technology (~8%) |

| Duration profile | Generally shorter maturities (~5y) and lower duration | Generally longer maturities (~10y) and higher duration |

| Credit quality profile | A3/BAA1 average rating according to Moody’s | A3/BAA1 average rating according to Moody’s |

| Yield level | Usually lower nominal yields in local currency terms | Typically higher nominal yields in local currency terms |

| Investor base | Strong regional participation from European insurers, pension funds and asset managers | Broader and deeper domestic investor base, plus global reserve and institutional flows |

| Portfolio diversification role | Useful diversifier due to different sector mix, shorter duration and relative valuation opportunities | Core credit allocation for many global portfolios |

Source: Bloomberg, as of 5 May 2026.

After accounting for hedging costs, Euro IG and USD IG have delivered very similar performance over the past 15 years, with cumulative returns of around 80% since 2010.

Total Return (Hedged in EUR)

Source: Bloomberg, Amundi. Data is as of 31 March 2026.

Why active management matters more in volatile markets

Another consequence of higher market volatility is that investors are increasingly returning to active management as a means to preserving capital and enhance returns. In an environment shaped by heightened geopolitical uncertainty and rapidly evolving flows, market demand is often far from fully rational and is not immune to behavioural biases, creating inefficiencies. For long-term investors, these dislocations can offer attractive opportunities to generate alpha.

Active management also allows for a more granular allocation across key risk factors, including duration, credit quality and subordination, enabling investors to adjust exposures dynamically as market conditions evolve. Even relationships that are typically considered stable, such as the correlation between interest rates and credit spreads, can change over time, creating further opportunities to express tactical views, hedge risk or enhance returns.

Why Amundi for Euro credit

Amundi has been an established player in the Euro Credit market since 1999 and currently manages approximately €380 billion in assets5. Its seasoned Euro Credit investment team is part of the broader Alpha Fixed Income platform, with total AUM of €833 billion5.

The team’s investment philosophy seeks to deliver consistent returns by navigating credit cycles effectively and capitalising on market inefficiencies. Its approach is dynamic, combining top-down and bottom-up analysis to inform portfolio construction and risk management.

Discover the Offer

Amundi Funds Euro Corporate Bond Select

Amundi S.F. Diversified Short Term Bond Select

Latest publications

- Source: Amundi, as of March 2026.

- Benchmark: Bloomberg Euro Aggregate Corporate Index (Ticker: LECPTREU). 5.68% cumulative total return over 11/03/2022 to 14/05/2026.

- Bloomberg Euro Aggregate Corporate Index (Ticker: LECPTREU)

- Bloomberg US Corporate Bond Index (Ticker: LUACTRUU)

- Source: Amundi, as of March 2026.

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 14/05/2026. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results.

Date of first use: 14 May 2026

Doc ID: 5491364