Key Takeaways

- To capture opportunities in this age of fragmentation, diversification* will need to go beyond traditional market capitalisation approaches and broaden from a regional perspective.

- We anticipate a larger role for Europe and Asia in portfolios, greater emphasis on structural themes, and a tilt towards the real economy.

- Active, global multi asset portfolios could offer a practical way to access multiple engines of growth, while keeping concentration risk at bay.

US market concentration may be facing a turning point

US equity concentration has defined markets for more than a decade, first in the aftermath of the 2008 financial crisis and later reinforced by the rise of artificial intelligence. The trend has also extended beyond equities, with strong inflows into US Treasuries reflecting investors’ search for yield and safety, while the US dollar has retained its dominant role in global trade invoicing and SWIFT payments.

This strength reflects clear structural advantages in the US, including higher productivity, a dominant technology sector, a supportive entrepreneurial culture and deep capital markets. These factors have enabled highly profitable companies with significant global revenue exposure to capture a growing share of earnings.

However, concentration can persist only while those growth advantages remain intact. As other markets begin to offer more attractive returns, the case for reallocation away from the US becomes more compelling. Signs of this shift were already visible in 2025, with MSCI World ex-US significantly outperforming its US counterpart1. At the same time, the US dollar has started to lose momentum as a safe haven, and we expect this weakness to continue gradually, supported by potential foreign capital outflows.

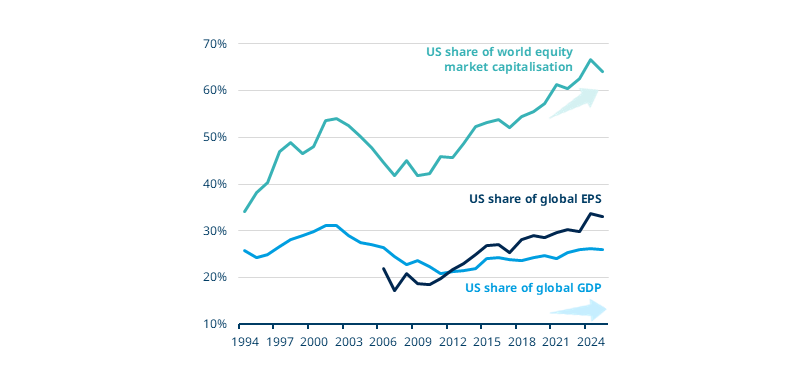

Markets have outgrown the real economy, particularly in the US

Source: Amundi Investment Institute, IMF, Bloomberg. Data related to GDP share is based on IMF data, market capitalization and EPS refer to MSCI US and MSCI World. Yearly data as of 2025.

Looking ahead: a greater focus on the real economy

As geopolitical rivalries intensify, global cooperation is weakening and supply chains are being reshaped by security and political constraints, particularly in strategic sectors such as critical minerals. The push for strategic autonomy is supporting higher defence and energy-related spending, but is also increasing fiscal pressure and debt sustainability concerns.

This points to a macro regime of uneven growth, higher debt and stickier inflation, with global growth continuing to shift from developed (DM) to emerging markets (EM). Policy and fiscal discipline have also strengthened in many EM countries, which are becoming more differentiated and offering greater exposure to technology, digital services and advanced manufacturing.

Europe also presents opportunities. The region needs to strengthen its defence, energy and digital capabilities, supporting higher investment and industrial upgrading. The AI investment cycle should also benefit the region through equipment, infrastructure and related industries, while further integration and deregulation should support companies across different market capitalisations.

Rethinking global diversification* from a regional and asset class perspective

The expected shift calls for a greater focus on diversification*. Over the medium to long term, US equities should still deliver solid returns, but leadership may be challenged, opening the way for a rotation towards Europe, Japan and emerging markets. Investors should therefore reduce concentration risk rather than abandon the US.

The same applies to bonds. Rising global debt levels, particularly in the US and some advanced economies, support a broader approach to diversification*. Sovereign bond investing is driven by three main objectives: income, low volatility and low correlation with equities, and US Treasuries are facing headwinds on all three fronts.

Meanwhile, EM debt continues to stand out for its combination of income and diversification*. For developed market investors outside the US, the case for strengthening domestic exposure is also becoming more compelling as local yields have improved.

Looking ahead, broadening exposure beyond the US is only part of the story. In an era of rupture, we also see opportunities in structural themes such as infrastructure and critical minerals, driven by AI demand and the energy transition, while gold should remain supported by policy uncertainty, constrained supply and central bank demand for additional reserves.

Structural themes will open diversification opportunities across regions and asset classes

| CMA Macro theme | Investment Implications | |||

| Opportunities amid rupture | Benefits domestic companies and rising EM powers (China, India) | ||

| AI could delay demographics' effect on growth | Benefits AI and tech beyond the US (first wave winner) - China and Asia as tech leaders, Europe industrial robotics | ||

| A delayed path towards Net Zero | Benefits commodity markets, critical minerals, clean tech, infrastructure, and green bonds | ||

| Strategic autonomy may enhance resilience | Benefits domestic companies, mainly in Europe | ||

| Debt and financial repression | Weaker dollar to benefit EM bonds. Euro bonds and Japanese bonds more appealing for domestic investors. Gold in demand as a diversifier for Central Bank reserves. | ||

Source: Amundi Investment Institute, June 2026.

Multi asset: an effective portfolio construction tool in a fragmented environment

Active multi asset portfolios could represent an effective way to navigate today’s fragmented market environment, characterised by elevated uncertainty, higher dispersion and ongoing policy shifts. Investor interest in this type of strategy is also reflected in the steady positive inflows seen in recent months2.

Equity-bond correlations have become less dependable, particularly in inflationary periods. In this context, multi asset strategies represent an evolution of the traditional 60/40 allocation: by combining multiple asset classes, they provide access to a wider set of opportunities across regions, sectors and styles, while helping to manage concentration risk.

A key advantage of multi asset investing is the flexibility it offers. Active portfolio management allows allocations to be adjusted as market conditions evolve, while disciplined security selection can help capture opportunities across different sources of return.

For investors considering exposure to multi asset strategies, strong due diligence and a well-defined, time-tested process are essential. The most compelling strategies are those managed by teams with the experience of keeping risk within clearly defined parameters and the ability to identify alternative sources of return before they become widely recognised.

For those seeking income distributions, whether to cover regular expenses or to generate additional income in retirement, our extensive product range also includes solutions that may help meet this need.

See our offer

AMUNDI FUNDS GLOBAL MULTI-ASSET CONSERVATIVE

FIRST EAGLE AMUNDI INTERNATIONAL FUND

AMUNDI FUNDS GLOBAL MULTI-ASSET TARGET INCOME

Read our news and insights

*Diversification does not guarantee a profit or protect against a loss.

Source: Amundi Investment Institute. Views are as of end June 2026 and are subject to change without prior notice.

[1] Source: MSCI, as of 31 December 2025. In 2025, the MSCI World ex-USA Index delivered a net return in USD of 31.85%, compared with 17.31% for the MSCI USA Index and 21.09% for the MSCI World Index.

[2] Lipper Alpha Insight | LSEG, “Everything Flows, Europe: May 2026”, June 23rd, 2026.

Marketing material for professional investors only

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 10 July 2026. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results.

Date of first use: 13 July 2026.

Doc ID: 5729937.