Convictions

Europe is at a turning point.

Watch our panel discussion to hear our experts on EU policy trajectories following recent meetings, their assessment of reform initiatives across the region, and the likely implications for fixed income and equity markets.

Speakers: Amaury D’Orsay, Head of Fixed Income & Money Market Investments, Amundi; Barry Glavin, Head of Equity, Amundi; and Didier Borowski, Head of Macro‑Policy Research, Amundi Investment Institute.

Although near term growth in Europe is modest, ongoing reforms and a shifting political landscape could prove transformative. Strategic policies - from energy and critical raw material security to defence cooperation and digital transformation - have laid the foundations for sustainable expansion.

A clear pathway to end Russian pipeline and LNG imports by early 2028, plus moves to explore pooled purchasing and stockpiling for selected raw materials, underscore this strategic shift.

The AI theme’s spread beyond the US should further boost Europe’s appeal.

Reasons for cautious optimism include possible EU institutional reform, a German fiscal pivot to support growth, and an industrial realignment around energy, infrastructure and defence.

Defence rearmament across the euro area is progressing unevenly: although there is a 40% joint procurement target for 2030, legal carve outs and national priorities still shape decisions. The 2026 test will be whether member states convert a shared threat assessment into coordinated spending and delivery schedules - shifting the focus from symbolism to readiness and production capacity.

Regulation is being adapted to reduce friction rather than dismantle legacy frameworks, with adjustments to timing and scope to preserve strategic direction. Attention is returning to the Single Market: removing services barriers, improving cross border data flows and streamlining standards and enforcement.

Sustaining Europe’s momentum requires resilient domestic demand, continued monetary support and timely policy execution. With higher debt and fiscal rules keeping the overall fiscal stance broadly neutral, easing inflation, moderating wage growth and below potential activity should allow central banks to remain relatively accommodative.

Europe’s journey continues as reforms, defence investment, and industrial policy redefine its investment landscape. We see opportunities emerging in euro credit, infrastructure and strategic autonomy themes that could reshape Europe’s financial ecosystem and help it move from modest growth toward a more self-sustaining long-term trajectory.

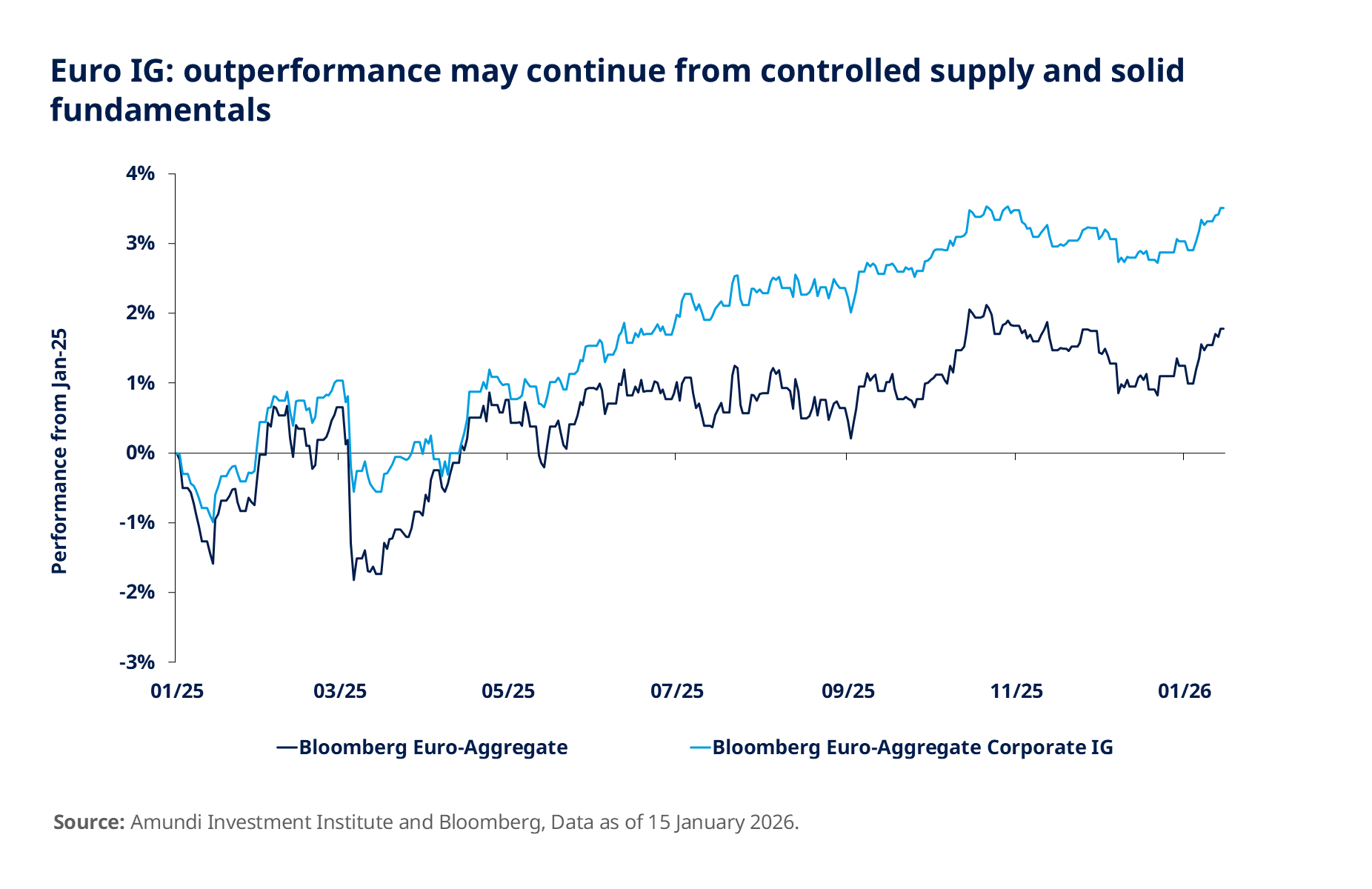

Narrowing 10–year Bund–Treasury spreads and an easing rate outlook should favour European fixed income over US peers. Greater predictability around fiscal rules and a larger market will likely draw more international demand. We remain constructive on peripheral sovereigns and see selective opportunities in investment grade credit.

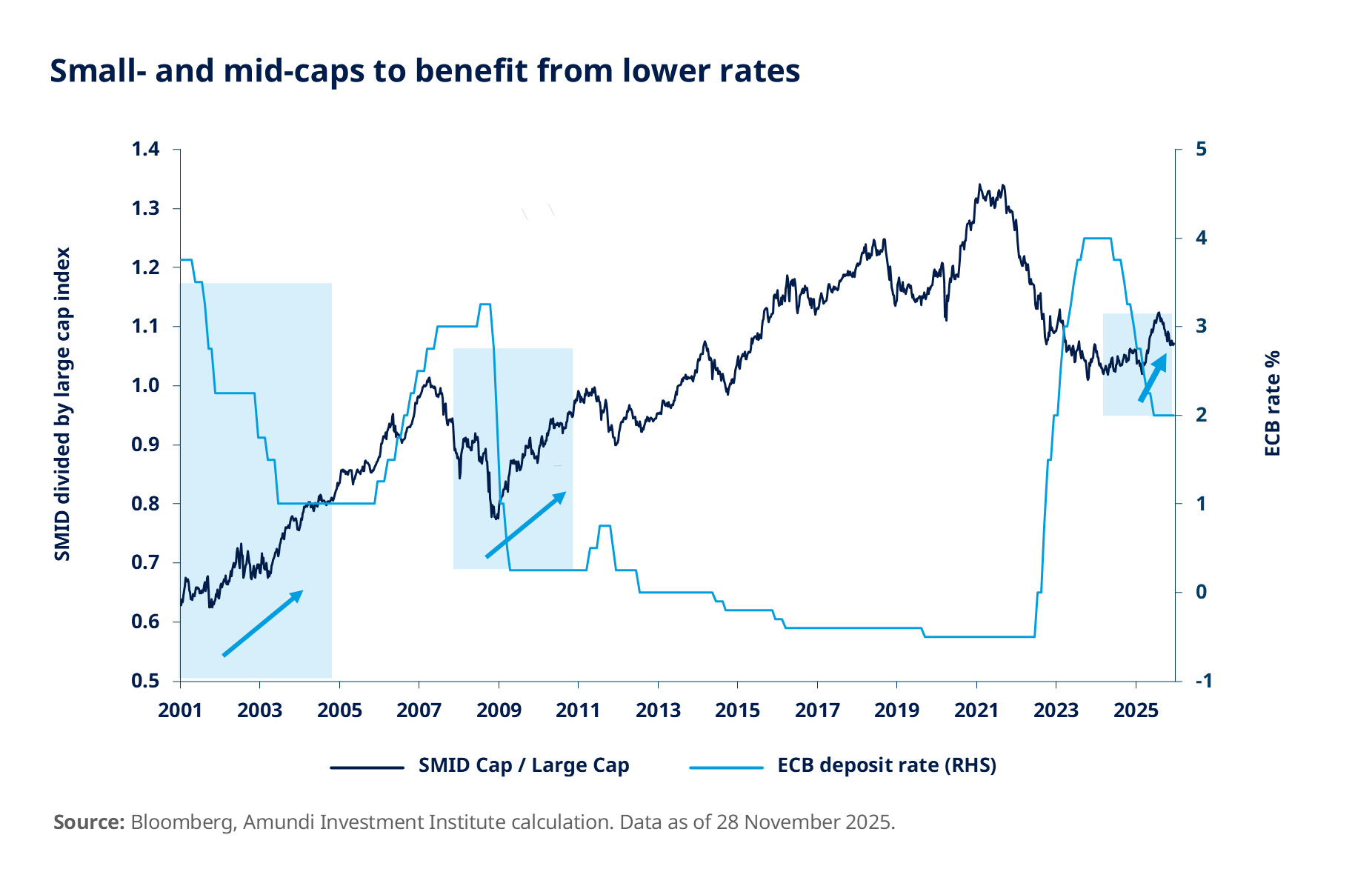

As domestic demand should drive growth, we prefer small and mid cap equities: roughly two thirds of their sales are domestic, making them less exposed to external shocks and US tariffs and more leveraged to Germany’s plans and Ukraine’s reconstruction. Their multi year valuation discount to large caps, together with potential ECB easing, provides further upside.

Increased infrastructure spending from the green transition and rising investment in AI should create additional opportunities. At sector level, higher security spending will benefit defence, while a steeper yield curve should support financials.

*Diversification does not guarantee a profit or protect against a loss.

Source: Amundi Investment Institute, 2026 Investment Outlook - Keep it turning, November 2025.

Marketing material for professional investors only

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S.A.S. and is as of 15 January 2026. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the author and not necessarily Amundi Asset Management S.A.S. and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product. This material does not constitute an offer or solicitation to buy or sell any security, fund units or services. Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results.

Date of first use: 15 January 2026

Doc ID: 5133119